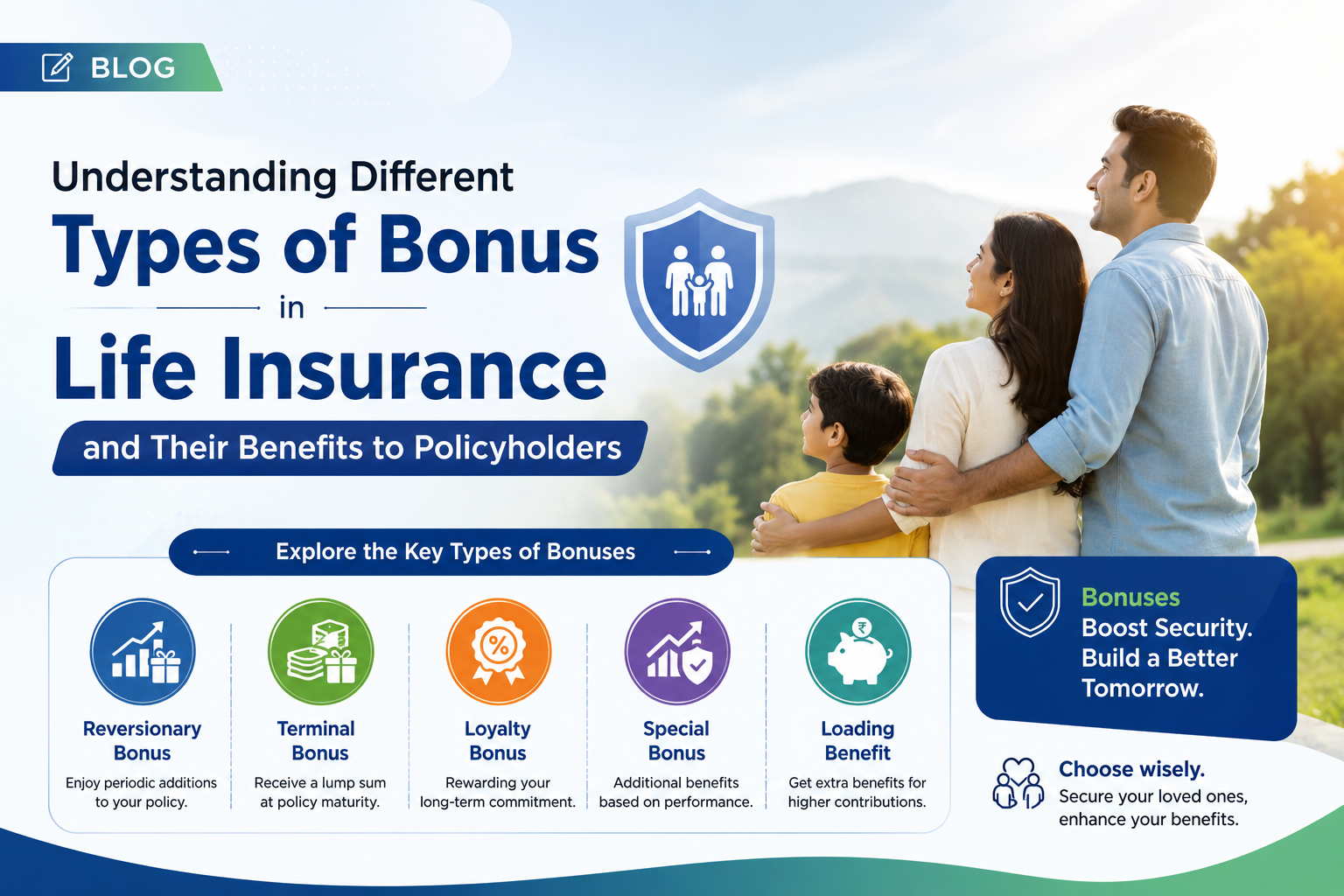

Understanding Different Types of Bonus in Life Insurance and Their Benefits to Policyholders

New Delhi: Life insurance is no longer viewed only as a financial protection tool for families. With changing consumer expectations and growing financial awareness, many policyholders are paying closer attention to additional benefits offered by insurance plans — particularly bonuses that can enhance overall returns.

Insurance experts believe that bonuses in life insurance policies can significantly improve maturity value and death benefits, especially in participating or “with-profit†plans. However, despite their importance, many buyers remain unfamiliar with the various types of bonuses available and how they impact long-term financial outcomes.

A life insurance bonus is generally an extra amount declared by insurance companies and added to eligible policies based on business performance, investment earnings, and overall profitability. These bonuses are mostly offered in traditional life insurance plans where policyholders participate indirectly in the insurer’s profits.

Financial advisors say understanding bonus structures is becoming increasingly important for customers looking to maximize policy benefits while balancing protection and savings goals.

Reversionary Bonus Remains the Most Common Form

Among the different categories, the reversionary bonus continues to be one of the most widely offered in life insurance plans.

Typically declared every year, this bonus gets attached to the policy and becomes payable at maturity or during claim settlement. Once added, it generally remains part of the policy benefits and is not withdrawn later.

Insurance providers usually offer two forms of reversionary bonuses — simple and compound.

In a simple reversionary bonus system, the calculation is based only on the original sum assured amount. This means the yearly addition remains linked to the base policy value rather than previously accumulated bonuses.

On the other hand, compound reversionary bonuses allow policyholders to benefit from growth on accumulated additions. Since future bonuses are calculated on both the original sum assured and earlier bonus amounts, policy value can grow more substantially over long durations.

Experts suggest that compound structures may offer stronger wealth-building potential for long-term investors.

Interim Bonus Ensures Fairness Between Annual Declarations

Since most insurers declare bonuses annually, there are situations where policies mature or claims arise before the next official declaration.

To address this gap, insurance companies may provide an interim bonus.

Industry professionals explain that interim bonuses act as temporary compensation to ensure policyholders or nominees do not lose out on profit-sharing simply because their claim occurred between two declaration periods.

Although generally smaller in value compared to annual bonuses, interim additions are seen as an important mechanism for maintaining fairness in policy settlements.

Terminal Bonus Rewards Long-Term Commitment

Another major category attracting attention among policyholders is the terminal bonus, often referred to as a final bonus.

Unlike yearly bonuses, terminal bonuses are paid only once, either at policy maturity or upon the insured individual’s death.

Experts note that insurers generally reserve terminal bonuses for customers who maintain their policies for extended periods. The amount depends on factors such as policy duration, premium history, financial performance of the insurer, and market conditions.

Long-term policyholders are often encouraged to continue policies until completion, as terminal bonuses can considerably increase the overall payout.

“Customers who stay invested for longer durations may receive substantial additions through terminal bonuses, depending on insurer performance,†financial planners say.

Guaranteed Bonuses Offer Greater Financial Predictability

For risk-conscious buyers, guaranteed bonuses are becoming increasingly attractive.

Unlike profit-linked bonuses, guaranteed bonuses are fixed and mentioned clearly in policy documents at the time of purchase. These benefits are not influenced by market performance or annual profits, providing policyholders with greater certainty regarding future returns.

Insurance advisors believe guaranteed bonuses appeal to individuals seeking predictable financial planning without exposure to fluctuations.

However, experts caution that while guaranteed benefits provide stability, they may sometimes deliver lower growth compared to performance-linked bonus plans during profitable market periods.

Cash Bonuses Provide Regular Income Support

Some insurance products also offer cash bonuses, allowing policyholders to receive bonus payouts directly rather than accumulating them within the policy.

These bonuses are usually paid periodically and can help individuals seeking supplemental income.

Retired persons or families looking for additional financial support often prefer cash bonus structures because they provide liquidity during the policy term.

However, financial planners advise customers to carefully evaluate whether immediate payouts align with long-term financial goals, as withdrawing bonuses may reduce overall maturity benefits.

Loyalty Additions Encourage Long-Term Policy Retention

Loyalty addition bonuses are another feature gaining popularity in long-term insurance products.

These bonuses are designed to reward policyholders who continue their plans for many years without interruption. Insurance companies generally add loyalty benefits after a specific duration, encouraging customers to avoid premature policy surrender.

The amount may vary based on premium contribution, tenure, and insurer performance.

Industry analysts believe loyalty additions not only strengthen customer retention but also enhance final policy value significantly.

Growing Awareness Among Buyers

As financial literacy improves across India, experts say customers are increasingly comparing insurance products not only on premiums and coverage but also on bonus history and long-term returns.

While bonuses can improve policy value considerably, advisors recommend that buyers read policy documents carefully and understand whether benefits are guaranteed or performance-linked.

With life insurance becoming an essential component of long-term financial planning, understanding bonus structures may help policyholders make more informed and rewarding investment decisions.