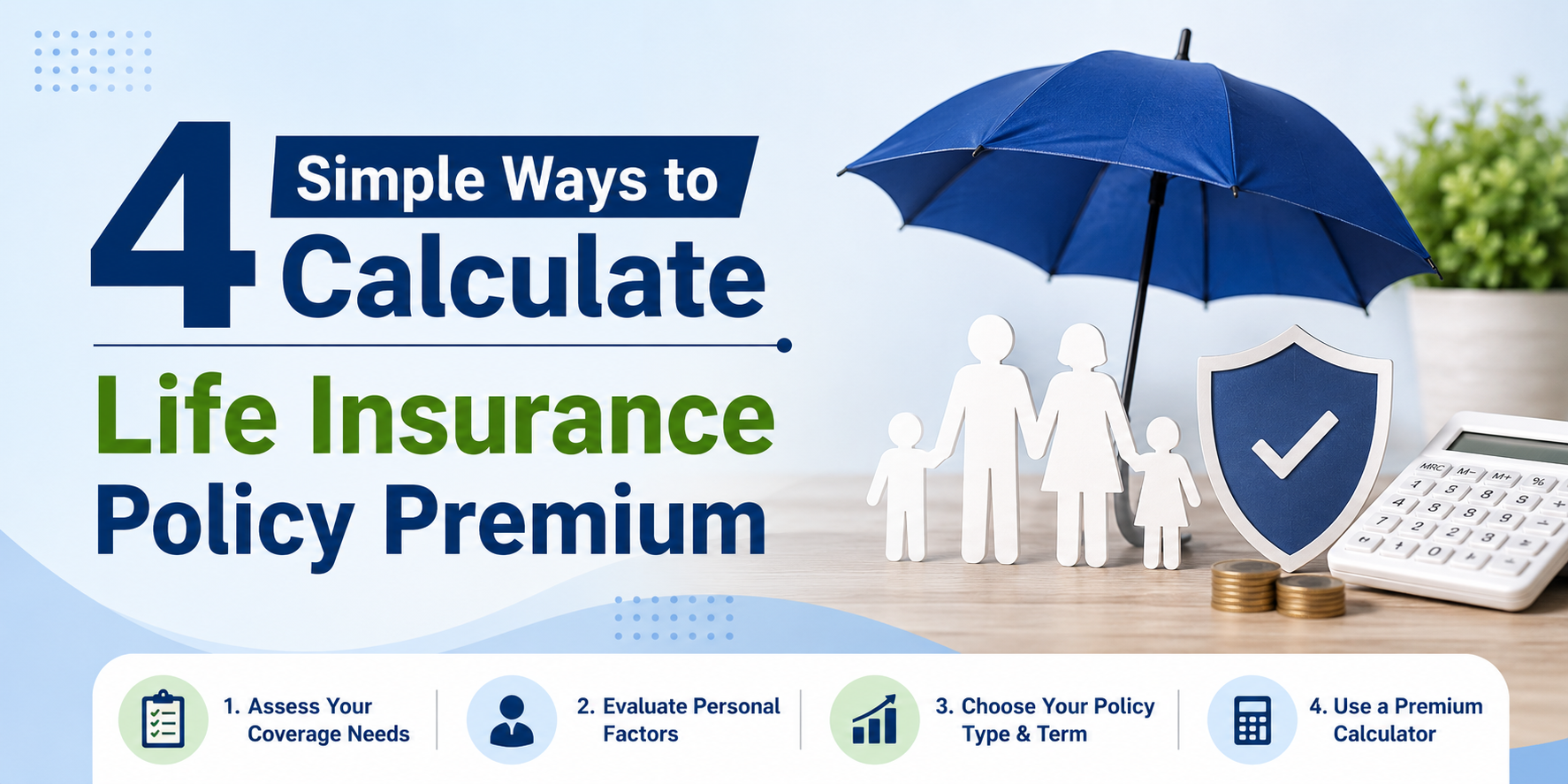

4 Simple Ways to Calculate Life Insurance Policy Premium

Life insurance helps provide financial support to your family when they need it most. Before buying a policy, it is important to understand how the premium amount is decided. A premium is the money you pay regularly to continue your insurance coverage.

The cost of a life insurance premium is not the same for everyone. Insurance companies calculate it by considering several factors such as age, health, coverage amount, and policy type. Understanding these methods can help you select a plan that matches both your needs and your budget.

Below are four common ways used to calculate life insurance policy premiums.

1. Premium Based on Age and Medical Health

Age is one of the biggest factors in deciding life insurance premiums. In most cases, younger people pay lower premiums because they are considered healthier and less risky to insure.

Health condition also matters when calculating the cost. Insurance companies often review medical history, existing illnesses, and lifestyle habits before deciding the premium amount.

Some important factors include:

- Current age

- Health history

- Smoking or alcohol habits

- Family medical records

- Weight and overall fitness

For example, a healthy person in their 20s may pay much less compared to someone in their 40s or 50s for the same insurance coverage.

2. Premium Based on Coverage Amount

The amount of financial protection you choose also affects your premium. This amount is called the sum assured, which is the money your nominee receives if something happens to you during the policy period.

Usually, larger coverage leads to higher premium payments.

For example:

- A ₹10 lakh insurance plan may have a smaller premium

- A ₹25 lakh plan may cost slightly more

- A life insurance plan with ₹1 crore coverage usually requires a higher premium payment due to the larger financial protection it offers.

When selecting coverage, it is important to consider family expenses, loans, children’s education, and future financial responsibilities.

3. Premium Based on Policy Type and Duration

The type of life insurance plan you choose can also change the premium cost. Every policy works differently and offers unique benefits.

Term Insurance Plans

These plans offer protection for a fixed period and usually have lower premiums because they mainly provide life cover.

Whole Life Insurance Plans

These policies provide protection for a lifetime, which is why premium costs are generally higher.

Endowment Policies

Such plans combine life cover with savings benefits. Since they offer maturity value, premiums may be more expensive.

ULIP Plans

Unit Linked Insurance Plans offer both insurance and investment opportunities, so premium costs may vary depending on selected funds.

The length of the policy term also matters. Longer plans may increase the total amount paid over time, although yearly premiums can sometimes be more manageable.

4. Calculating Premium Through Online Tools

Many insurance companies now provide online premium calculators to help customers estimate policy costs quickly.

These calculators ask for details such as:

- Age

- Gender

- Income level

- Smoking habits

- Desired coverage amount

- Policy period

Within minutes, you can get an estimated premium amount. These online tools are useful for comparing different insurance plans and finding one that suits your budget.

They also save time by helping you understand expected costs before speaking with an insurance advisor.

Other Factors That May Affect Premium Costs

Apart from the main calculation methods, some extra factors can influence premium pricing:

- Job risk level

- Existing medical conditions

- Lifestyle choices

- Adventure or risky hobbies

- Payment option selected (monthly or yearly)

- Additional policy benefits or riders

People with healthy habits and low-risk lifestyles often receive better premium rates.

Conclusion

Life insurance premiums are calculated using several important factors including age, health condition, coverage amount, policy type, and policy duration. By understanding these four methods, you can make a better decision while choosing a life insurance plan.

Before purchasing any policy, compare different options, estimate premium costs, and choose a plan that gives proper financial protection without putting pressure on your budget. A well-planned insurance policy can help secure your family’s future financially.