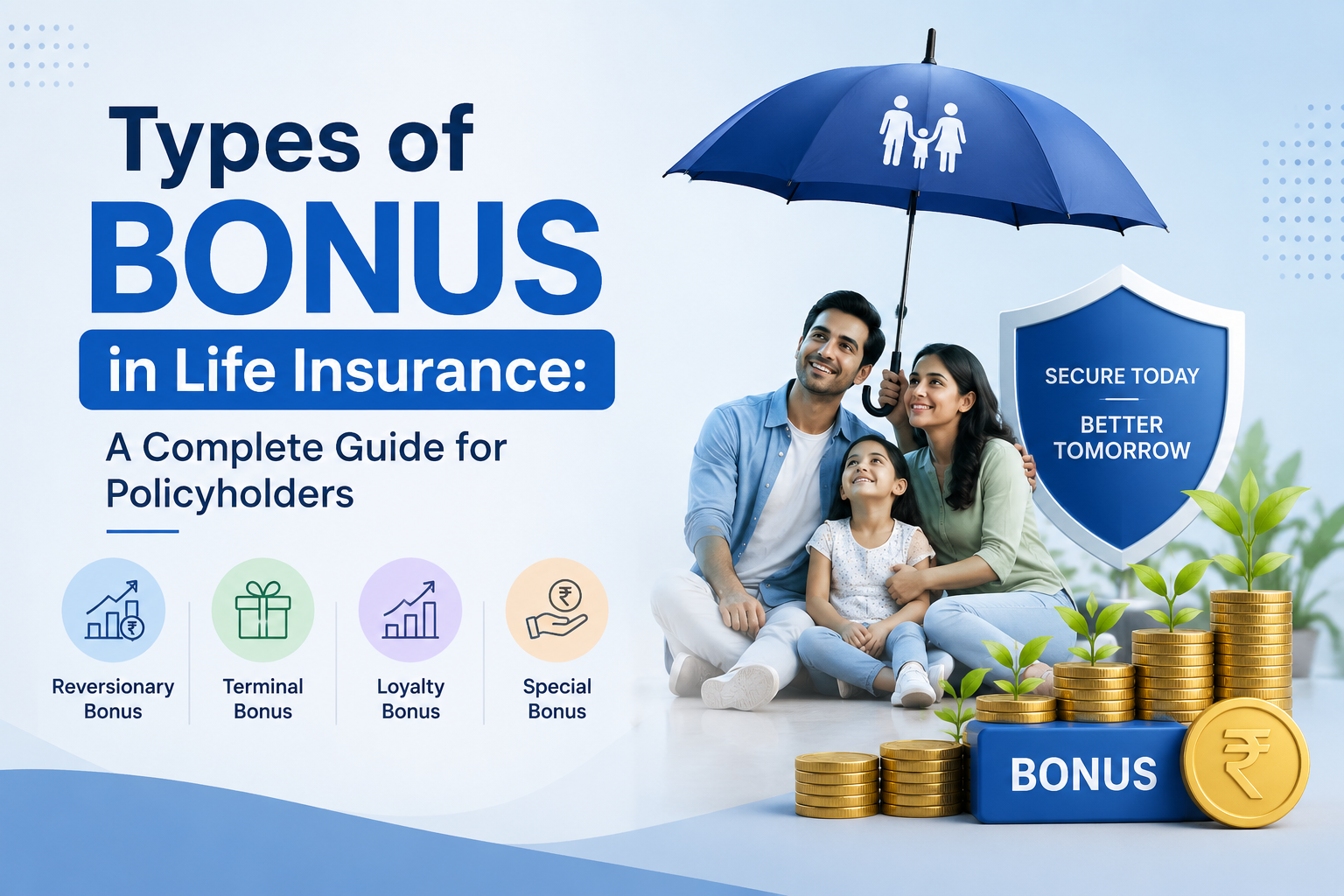

Types of Bonus in Life Insurance: A Complete Guide for Policyholders

Life insurance is primarily designed to provide financial security to loved ones, but many policies also offer additional benefits in the form of bonuses. These bonuses can significantly increase the value of a policy over time, making life insurance not only a protection tool but also a financial asset. However, many people are unaware of how these bonuses work and the different categories available in life insurance plans.

If you are planning to buy a life insurance policy or already own one, understanding the types of bonuses can help you better evaluate your policy benefits and expected returns.

What Does Bonus Mean in Life Insurance ?

In life insurance, a bonus refers to an extra amount declared by an insurance company and added to eligible policies. These bonuses are generally available in participating or “with-profit” insurance plans. Since policyholders contribute premiums that insurers invest, a share of the profits may be distributed back through bonuses.

The amount of bonus depends on factors such as investment earnings, financial performance of the insurer, claim ratios, and business growth. While some bonuses are guaranteed, others depend on company performance and are announced periodically.

Let’s understand the major kinds of bonuses offered in life insurance policies.

1. Simple Reversionary Bonus

One of the most common bonuses in traditional life insurance plans is the simple reversionary bonus. Insurance companies usually declare this bonus every year and add it to the policy benefits.

This bonus is calculated on the original sum assured amount and does not increase based on previously added bonuses. Once declared, it generally remains attached to the policy and is payable at maturity or during a death claim.

For instance, if your policy has a sum assured of ₹8 lakh and the insurer declares a yearly bonus rate, the calculation is based only on the initial insured amount rather than accumulated benefits.

This type of bonus helps gradually improve the maturity amount over the policy period.

2. Compound Reversionary Bonus

The compound reversionary bonus works in a slightly different manner compared to the simple version. In this case, the bonus is calculated not only on the original sum assured but also on bonuses accumulated in previous years.

Because of this compounding effect, the value of the policy grows faster over time.

For long-term investors, compound bonuses can create a much larger corpus at maturity, especially when policies remain active for several years. This makes them attractive for individuals seeking both insurance coverage and savings growth.

3. Interim Bonus

Insurance companies usually announce bonuses once every financial year. But what happens if a policyholder’s claim occurs before the next declaration period?

This is where an interim bonus becomes relevant.

An interim bonus is provided when a policy matures or a claim arises between two annual bonus announcements. It acts as temporary compensation so that policyholders or beneficiaries do not miss out on the profits earned during that period.

Although this bonus is usually smaller than annual declared bonuses, it ensures fairness in policy settlements.

4. Terminal Bonus

A terminal bonus is often viewed as a reward for policyholders who continue their plans until the end of the term.

Also called a final bonus, this is paid only once — either at policy maturity or upon the death of the insured person. Unlike annual bonuses, it is not credited every year.

Insurance providers generally offer terminal bonuses to long-term policyholders, especially those who have maintained their policies consistently over many years.

The amount may vary depending on:

- Duration of the policy

- Premium payment history

- Financial health of the insurer

- Overall investment performance

A terminal bonus can considerably increase the final policy payout, especially in long-duration life insurance plans.

5. Guaranteed Bonus

As the name suggests, a guaranteed bonus is fixed and promised in advance by the insurer.

This type of bonus does not depend on the company’s profit performance or market conditions.

Guaranteed bonuses offer predictability and financial clarity because policyholders know in advance what additional benefit they will receive if the policy conditions are fulfilled.

People who prefer stable and low-risk financial planning often choose policies that include guaranteed bonuses.

However, since these bonuses are fixed, they may not grow as much as performance-based bonuses in highly profitable years.

6. Cash Bonus

Certain life insurance policies allow bonuses to be paid directly in cash rather than accumulating within the policy.

Instead of increasing the maturity value, the insurer provides the declared amount to the policyholder at regular intervals, usually yearly.

This can be useful for people who need periodic income or extra financial support during the policy term.

For example, senior citizens or individuals seeking supplementary cash flow may prefer this option.

However, taking bonuses as cash may result in a comparatively lower final maturity amount because the bonus is not retained within the policy for future growth.

7. Loyalty Addition Bonus

A loyalty addition bonus is an extra benefit offered to policyholders who continue their investment for an extended period, rewarding them for long-term commitment to the policy.

Insurance companies often add this bonus after a specific number of years, encouraging customers to continue their policies without surrendering them early.

The bonus amount depends on factors such as:

- Policy duration

- Total premium contribution

- Policy type

- Company performance

Loyalty additions can meaningfully improve the overall maturity proceeds and are especially valuable in long-term savings-oriented insurance plans.

Why Are Bonuses Important in Life Insurance?

Bonuses make life insurance policies more rewarding by increasing the overall financial benefit. Instead of receiving only the sum assured, policyholders may receive additional amounts that boost long-term wealth creation.

Some key benefits of bonuses include:

Higher Maturity Benefits

Accumulated bonuses can increase the final payout significantly.

Better Family Protection

In case of an unfortunate event, added bonuses may improve the death claim amount received by beneficiaries.

Encouragement for Long-Term Savings

Many bonuses reward policyholders for staying invested for extended periods.

Wealth Accumulation

Certain bonus structures help policyholders build a larger financial corpus over time.

Things to Consider Before Choosing a Policy

Before purchasing a bonus-based life insurance plan, it is important to evaluate several aspects:

- Check whether the bonus is guaranteed or non-guaranteed

- Review the insurer’s past bonus declaration record

- Understand how bonuses are calculated

- Compare long-term returns with other financial products

- Read policy terms carefully before investing

A policy with attractive bonus features may offer better value in the long run.

Conclusion

Bonuses in life insurance can play a major role in enhancing the financial benefits of a policy. Whether it is a reversionary bonus, terminal bonus, guaranteed bonus, or loyalty addition, each category contributes differently to policy growth and protection.

Understanding these bonus structures helps policyholders choose suitable insurance products that align with their financial goals. Instead of focusing only on the sum assured, considering bonus benefits can give a clearer picture of the total value a life insurance plan may provide over time.